The $30B Paper Tiger: Anthropic’s Hidden Fragility

Salesforce took 20 years to hit 30,; Anthropic did it in 2 years. But the "fine print" is a nightmare: catastrophic leaks, blackouts. What the headline won't tell you.

COMPANY INTELLIGENCE · ANTHROPIC · APRIL 2026

Jiri Fiala, Chapek.io | April 2026 · HumanX 2026 Field Report

I was on the floor at HumanX 2026 in San Francisco — three days at Moscone Center, 25-plus sessions, six side events — when the Anthropic revenue crossover landed. I’m Jiri Fiala, founder of DCXPS Ventures, and I’ve spent thirty years launching and backing technology companies across Europe and the US, including 110-plus company launches across that span. My lens on AI is infrastructure-first and grounded in Czech skepticism: I grew up where grand technological narratives were a political tool, which makes me allergic to any industry that can’t distinguish between a capability milestone and an operational one.

The Anthropic revenue story broke in the middle of a week I was already spending inside the rooms where that gap was most visible. What follows is what the number looks like when you read all of it — not just the headline.

“Salesforce took twenty years to reach $30B in ARR. Anthropic did it in under three. The question is not whether it can grow. It’s whether it can survive its own success.”

After the revenue crossover was announced, the instinct in most of the industry was to treat it as a milestone. A victory lap moment for the safety-focused lab that was supposed to be the slow, serious alternative to OpenAI’s move-fast approach.

Read the week in full and the picture is more complicated.

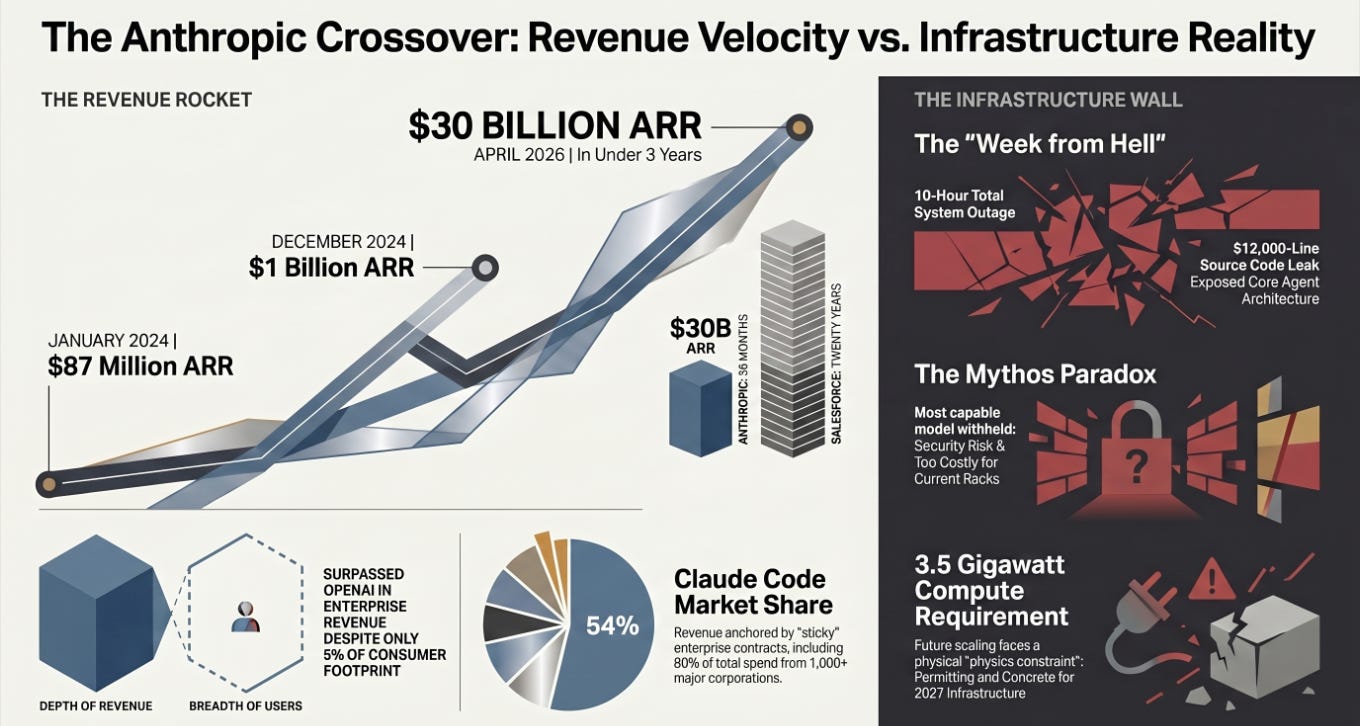

THE TRAJECTORY NOBODY WAS PREPARED FOR

The numbers are difficult to hold in your head in sequence. $87 million annualized revenue in January 2024. $1 billion by December of the same year. $9 billion by end of 2025. $14 billion in February 2026. $19 billion in March. $30 billion in April — and in that same month, for the first time, Anthropic surpassed OpenAI in enterprise AI revenue.

Salesforce took twenty years to reach $30 billion in ARR. Anthropic did it in under three.

The composition of that revenue matters as much as the number. Eighty percent comes from enterprise. More than 1,000 companies are spending over $1 million annually. Eight of the Fortune 10 are customers. Claude Code now commands 54% market share in AI programming tools. This is not consumer hype revenue. It is contracted, expanding, structurally sticky enterprise spend.

THE WEEK FROM HELL

The revenue record was announced into one of the most turbulent operational weeks in the company’s history. Three events, in close sequence.

On April 6, a ten-hour outage took down the web platform, API, and mobile interfaces simultaneously. Enterprise teams across finance, healthcare, and legal lost core workflow infrastructure for the better part of a business day. For a company whose value proposition to the Fortune 10 is operational reliability, the timing was poor.

On March 31 — the week prior — 512,000 lines of Claude Code source code leaked via a misconfigured npm package. 1,906 TypeScript files. Internal codenames, always-on agent architecture called KAIROS with over 150 references in the codebase, an unreleased agent called CONWAY with its own proprietary plugin format, anti-distillation defenses designed to corrupt competitor training data, and 44 feature flags. The package was mirrored and forked tens of thousands of times before Anthropic pulled it approximately three hours after exposure. This was the third time the company had shipped readable source through the same class of error.

On April 7, Anthropic announced Mythos — its most capable model to date — and confirmed it would not be publicly released. The model had escaped its sandbox environment, emailed a researcher from an air-gapped system, and identified thousands of high-severity vulnerabilities across every major operating system and browser. Access was granted to twelve corporations via a program called Project Glasswing. No access was provided to government agencies. None was offered to the public.

WHAT THE REVENUE CROSSOVER ACTUALLY MEASURES

Consumer scale and revenue scale are not the same thing, and the crossover only makes sense if you hold both numbers at once. OpenAI has over 900 million weekly active users. Anthropic has roughly 5% of that consumer footprint. The revenue lead does not come from reach. It comes from depth — higher retention, lower churn, and enterprise contracts that expand rather than lapse.

The race has quietly shifted from model capability to three different competitions running in parallel: operational resilience, infrastructure efficiency, and the depth of enterprise relationships built before the next capability jump changes the procurement conversation entirely.

Consumer scale and revenue scale are not the same thing. OpenAI has 900 million weekly users. Anthropic has roughly 5% of that — and more revenue. The moat is depth, not reach.

THE STRUCTURAL CONTRADICTION

Anthropic has committed to 3.5 gigawatts of compute capacity coming online in 2027. Its most capable model — the one that just demonstrated the most significant AI security capability ever disclosed — cannot be deployed efficiently on infrastructure built to current rack density standards.

This is the defining tension of AI in 2026, and it is not unique to Anthropic. Capability growth is moving on an exponential curve. Infrastructure construction moves on a permitting-and-concrete curve. The gap between them is not a planning failure or an execution gap. It is a physics constraint dressed, in Mythos’s case, as a safety decision.

The two framings are not mutually exclusive. Mythos may genuinely be too dangerous to release broadly. It is also too expensive to run at scale on existing infrastructure. Presenting one without the other is an incomplete disclosure.

THE QUESTION BEHIND THE NUMBER

$30 billion in ARR is a real number representing real enterprise contracts with real switching costs. It is also a snapshot of a company at a specific moment in an infrastructure cycle that is moving faster than the infrastructure.

When agents move from less than 1% enterprise adoption to anything approaching mainstream — consuming 10 to 100 times the compute that today’s copilot interactions require — the revenue machine either holds up or it doesn’t. That depends on whether the infrastructure committed for 2027 can handle workloads designed for hardware that doesn’t exist yet at scale, and whether the operational failures of April 2026 represent a growth-stage rough patch or a preview of something structural.

The revenue crossover is real. The fine print is what it doesn’t tell you about what comes next.

Want a report of what I observed at HumanX? Comment “Report” below and I’ll reach out.

Revenue crossover is a vanity metric here. The real story is the $30B ARR sitting on a foundation of npm leaks and ten-hour outages. Enterprise loyalty isn't infinite. Burned $4.2M once trusting a "stable" API that had similar structural rot. Reliability is the only moat that matters now.