Prediction 9 Revisited: I Said Energy Would Become AI's Binding Constraint and Compute Would Decentralize Toward Power. It Did. I Bet My Company On It.

Waymo's 2026 expansion map is my January 2025 prediction rendered in geofences.

Of all thirteen predictions I made in January 2025, this is the one I didn't just write down. I reorganized my company around it.

Full disclosure before I grade myself: this prediction became the thesis of everything I now build and write. So read my self-assessment with that bias in mind. I'll keep it data-anchored to make up for it.

Prediction nine: rising power demands for large-scale AI intensify scrutiny from regulators, investors, and the public. Massive centralized data centers draw criticism for inefficiency. Decentralization — edge computing, renewable integration, asynchronous scheduling — emerges to distribute energy draw.

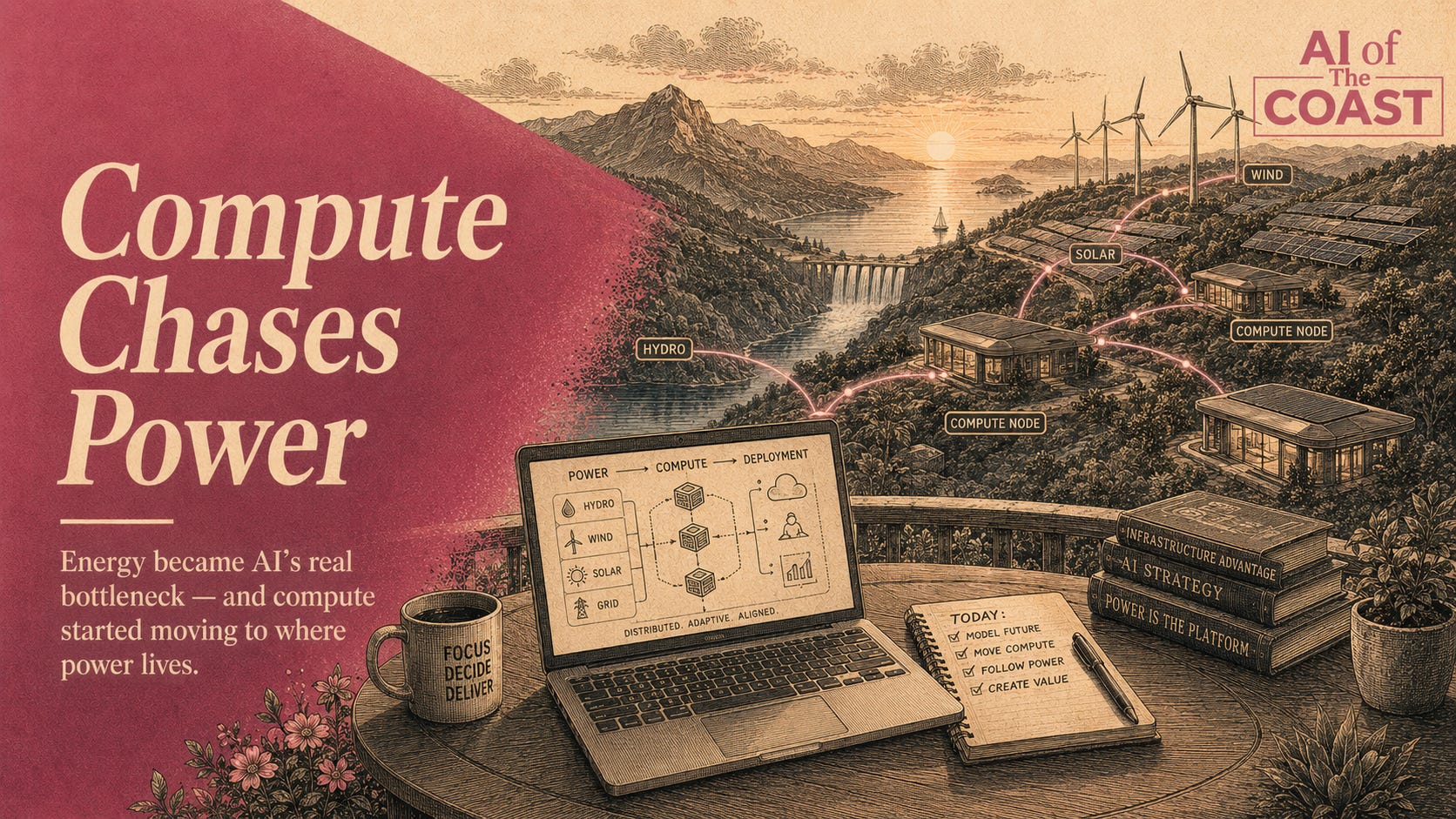

My favorite spin-off: 'Mobile AI Data Centers,' containerized compute clusters anchored on or near renewable power sites, harvesting clean or stranded energy at the source.

Energy became THE constraint. Not a constraint. The constraint.

The numbers that vindicated this prediction are almost violent. The IEA's April 2025 Energy and AI report put global data-center electricity consumption on track to exceed 1,000 terawatt-hours by end of 2026 — Japan's entire annual consumption. Bloom Energy's January 2026 report: US data-center demand nearly doubling from 80 GW in 2025 to 150 GW by 2028. Wood Mackenzie (May 2026): US capacity needs going from 24 GW to 100 GW by 2030. Five tech companies spent $400B+ on AI infrastructure in 2025; the IEA projects that rising another 75% in 2026.

1,000+ TWh — global data-center electricity by end 2026, equal to all of Japan (IEA)

80→150 GW — US data-center demand, 2025 to 2028 (Bloom Energy)

$400B+ — 2025 AI infrastructure capex by five companies (IEA)

1,037% — PJM capacity price increase for the 2026-27 delivery year

And the scrutiny I predicted?

The PJM Interconnection capacity auction for the 2026-2027 delivery year cleared at $329.17 per megawatt-day, up from $28.92 the prior year — a 1,037% increase, with data-center growth explicitly named as a major driver.

Community opposition has blocked tens of billions in data-center projects. Transformer lead times hit 160 weeks. The grid became the bottleneck. Exactly as predicted: power-grid stability and the scramble for real estate near generation became the defining infrastructure fight.

The centralized-inefficiency critique: validated harder than I expected

I said centralized mega-facilities would draw criticism for inefficiency. What I underestimated is how the inefficiency would compound with the GPU density curve. Facilities designed for 20-25 kW racks are being asked to serve workloads needing 200-250 kW per rack.

The mismatch means a lot of capital is going into buildings that are structurally under-equipped before they open.

The centralized model isn't just drawing criticism for energy inefficiency — it's drawing it for architectural obsolescence, which is a sharper version of the point I made in January 2025.

Mobile/modular data centers: from 'my favorite spin-off' to my actual work

This is the part where prediction became vocation. My January 2025 'Mobile AI Data Centers' concept — containerized clusters at renewable or stranded-energy sites, modular, pay-as-you-scale, resilient through distribution — is now the core infrastructure thesis I spend my days on.

The logic only got stronger: if power is the binding constraint and the grid can't be rebuilt fast (20-40 year infrastructure lifespans against an 18-month compute-density cycle), then the rational move is to bring modular compute to where the power already is, rather than dragging power to where someone wanted to build a cathedral.

I'm not going to pretend the modular model has won — centralized hyperscale is still where the headline capex goes.

But every structural pressure I named in January 2025 pushes toward distribution, and the gap between what hyperscale promises and what the grid can deliver is the widest it's ever been.

The next 12 months: the stranded-asset reckoning begins

My forecast for May 2027: the first major hyperscale facility is publicly acknowledged as under-equipped for the GPUs it was meant to host — a stranded or stranded-ish asset, built for a density that frontier workloads have already outrun.

When that happens, the conversation flips from 'how fast can we build gigawatt campuses' to 'how do we avoid building obsolescence.'

Watch energy-sovereign and behind-the-meter compute go from fringe to portfolio strategy.

As capacity prices stay elevated and interconnection queues run 5+ years, compute that brings its own power stops being a niche play and becomes the only way to deploy on a reasonable timeline.

The constraint I named in January 2025 doesn't ease in the next year. It tightens, and the tightening is the opportunity.

Grade: hit, and the most consequential one I made — not because it was the hardest call, but because it was the one I was willing to bet on. Predicting the constraint is cheap. Reorganizing around it is the expensive part, and the only part that pays.

____

Sources: original forecast (Jan 6 2025); IEA Energy and AI report (Apr 2025); Bloom Energy infrastructure report (Jan 2026); Wood Mackenzie (May 2026); PJM 2026-27 capacity auction; Quanta Services ($2.4T grid opportunity); transformer lead-time and interconnection-queue data 2026.

Is a modular data center going to be bigger or smaller than a wind turbine blade? Lengthwise.