The AI Bubble Callers: Not the ones with billions of $ and actually using it. I am. Amongst the others:)

If AI is a bubble, it's the first bubble in history where the skeptics hold the opinions and the believers hold the keyboards.

I spent last week doing something embarrassing for a man who has founded 110+ companies. I rebuilt a financial reconciliation pipeline myself, at night, with an AI agent, line by line. Not because nobody on my team could do it. Because I could no longer allocate capital into a stack I couldn't feel with my own hands. More on that later, because it turns out I'm not the only greybeard back at the keyboard.

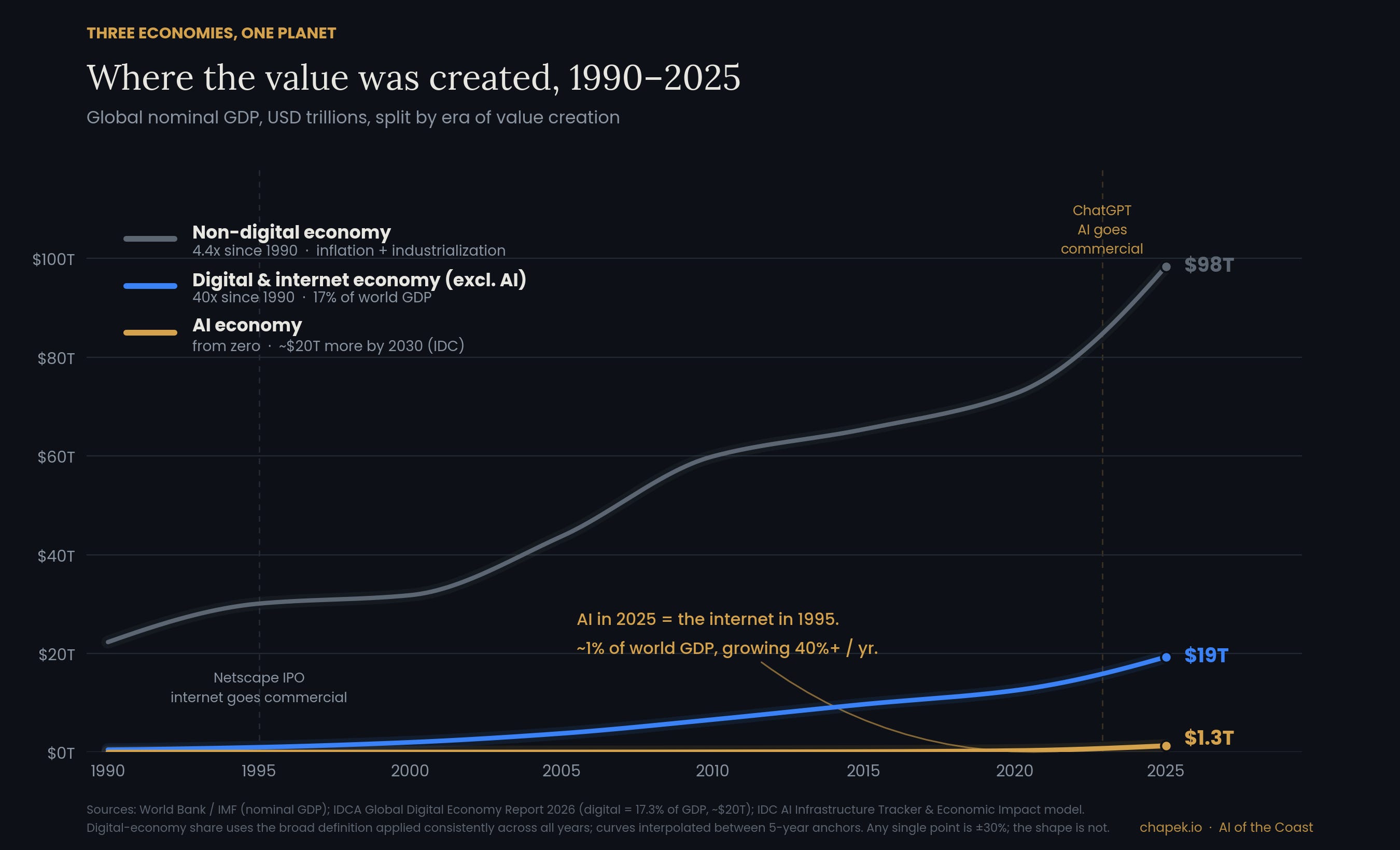

First, the chart everyone is misreading.

Take global GDP since 1990 and split it into three economies. The non-digital economy — steel, food, construction, everything your grandfather would recognize — grew from roughly $22 trillion to $98 trillion. A 4.4x, and most of that is inflation plus China industrializing. The digital economy went from about half a trillion to $20 trillion, now 17.3% of world GDP per IDCA's 2026 research. That's 40x. Same planet, same 35 years, ten times the growth multiple.

The third line is AI. Today it's maybe $1.3 trillion — roughly 1% of world GDP. On the chart it looks like a rounding error hugging the x-axis.

That is exactly what the internet line looked like in 1995.

The bubble question is the wrong question

Here is what the bubble callers get right: valuations are stretched, capex is enormous, and most enterprise pilots fail. Fine. All true in 1999 too.

Here is what they get wrong: they think the equity bubble and the value creation are the same event. They never are. The dot-com crash vaporized $5 trillion in market cap between 2000 and 2002. Cisco shareholders lost 80% and waited two decades to break even. And the infrastructure that capital paid for — the fiber, the data centers, the protocols — went on to carry a digital economy now worth $20 trillion a year. Every year. Forever.

The bubble was real.

The value was realer.

Those are two different charts, and confusing them is how you end up smugly correct in 2001 and structurally poor by 2010.

There's also a mechanical difference this cycle that the 1999 comparison ignores. The dark fiber laid in the telecom boom sat mostly unlit for years — capacity waiting for demand that hadn't arrived. GPU capacity today is the opposite problem: demand queues for supply. IDC clocked AI infrastructure spending at nearly $90 billion in Q4 2025 alone, 62% year-over-year growth, and projects $487 billion for 2026 with the market passing $1 trillion by 2029. The St. Louis Fed measured information-processing equipment contributing 0.90 percentage points to US real GDP growth in Q1 2025 — more than two standard deviations above its long-run average. You can argue about whether Nvidia is worth its multiple. You cannot argue with utilization.

Could specific equities crater? Absolutely. Will some of the circular vendor-financing deals end in tears? Some will. Does any of that stop the red line on my chart from doing in one decade what the blue line needed three to do? IDC models AI driving 3.5% of global GDP by 2030 with $19.9 trillion of cumulative impact. Even if they're off by half, it's the largest value migration of your working life.

Disclosure, because I do this inline and always will: I run DCXPS, we build modular intelligence factories on stranded power, and our first $45M unit commissions in January 2027. I am talking my book. The book is public; check the math yourself.

The founders went quiet and started typing

Now the part that should actually worry the bubble callers.

The loudest bubble arguments come from people whose relationship with AI is a stock ticker and a podcast feed. Meanwhile, the people with the longest track records of being early went silent about eighteen months ago and did something almost nobody predicted.

They started coding again.

Garry Tan runs Y Combinator — arguably the best seat in the world for pattern-matching what's next. He didn't write a memo about agents. He published his personal agentic toolchain and the receipts: three production services and forty-plus shipped features in sixty days, part-time, a self-measured ~810x increase over his 2013 coding pace. Andrej Karpathy, one of the defining engineers of the deep-learning era, put it in eleven words this year: "I don't think I've typed a line of code since December." The man who taught half the industry to program stopped typing — and became more productive.

I watch the same thing every week from my own seat. Fund partners asking for agent-tool licenses before their analysts do. Founders in their fifties who last shipped code when Nokia was a phone company, now running overnight agent sessions. A generation of operators who spent twenty years delegating implementation suddenly demanding to touch it again.

Why?

Because the abstraction penalty flipped.

For thirty years, the rational move for a capital allocator was to stay high in the stack: strategy up here, implementation down there, a management layer translating between. AI collapsed the translation layer. When one person with agents can do what previously required a team, the person who can operate the agents directly holds an information advantage over the person reading their summary. The founders re-learning the stack aren't nostalgic. They're refusing to price an asset class through an interpreter.

Klarna showed the corporate version: its AI assistant reportedly handled two-thirds of customer-service chats in its first month, work equivalent to roughly 700 full-time agents. Accenture showed the brutal version — 11,000 positions eliminated between June and August 2025 while revenue rose 7% to $69.7 billion and GenAI bookings jumped from $3 billion to $5.1 billion. Read that pair of numbers again. Revenue up, humans down, AI bookings nearly doubled. That's not a company betting on a bubble. That's a company repricing labor in public.

Follow the money into the ground

If this were a speculative mania, the money would concentrate in the most liquid, most flippable layer: model-company equity, AI-labeled SaaS, tokens of things. Some does. But look at where the largest checks actually land: Meta committing $600 billion to data centers and AI infrastructure through 2028. Microsoft's $80 billion year. Google's $85 billion. Nvidia and TSMC forming a $500 billion manufacturing partnership. Sovereigns in the Gulf posting the fastest regional infrastructure growth on earth in Q4 2025.

Concrete.

Transformers.

Cooling loops.

Twenty-year assets.

Speculators buy what they can sell by Friday.

This capital is buying things that take years to energize, in a grid environment where 2,300+ GW sits stuck in US interconnection queues and historically about 14% ever reaches commercial operation, where PJM capacity prices went from $28.92 to $329.17 per MW-day in one auction cycle — an 11x. Nobody pours patient capital into a decade-long power problem because a chatbot demo impressed them. They do it because they've concluded compute is the scarce input of the next economy and electricity is the scarce input of compute.

The model layer, meanwhile, is getting squeezed from both ends — commoditized from below by open-weight releases, and increasingly subject to government direction from above. When the middle of a stack compresses, value migrates to the layers that can't be copied with a download: the physical infrastructure underneath and the orchestration on top. The smart money read that memo early. It's why the checks go into the ground.

The wealth landscape, 2031

So play it forward five years. Three shifts, and they compound.

One:

the leverage ratio per human breaks.

WhatsApp previewed this in software — 55 employees, $19 billion exit. Agentic AI extends the decoupling from product into operations, and the spread will be violent. Traditional infrastructure operators run $0.5–1.5M revenue per employee. AI-native operators will run an order of magnitude more, and the gap lands as margin. Inside DCXPS we treat this as the whole thesis: four humans, an agent fleet, a $45M asset, and a standing rule that any agent that can't beat 20% of a loaded human's cost in 90 days gets retired. Most agents fail that bar. The ones that pass change the unit economics permanently.

Two:

energy owners become the new landlords.

For a century, owning generation was a regulated-utility business — safe, dull, 8% returns. When compute demand grows 23% annually against 3% grid growth, every megawatt of connected, available power becomes optionality on the fastest-growing industry in history. The family offices quietly buying brownfield sites near substations understand this. The ones still debating "bubble or not" on panels do not.

Three:

the divide moves from capital-vs-labor to fleet-vs-hours.

The internet era's wealth question was: do you own equity or earn wages? The AI era's question is: do you command agents or compete with them? A single fluent operator directing a fleet compounds output at machine speed. A brilliant professional selling hours competes against a marginal cost falling 60–75% per hardware cycle. This is why the founders went back to the keyboard, and it's the most honest career advice on the internet right now, free of charge: the window where hands-on agent fluency converts into structural wealth is open today the way HTML fluency was open in 1996.

It will close the same way.

Quietly.

Around the time your company hires its first "VP of Agent Operations" and the skill becomes a job description instead of an edge.

The uncomfortable close

In 2000, the correct call was: the stocks are overpriced and the internet is underestimated. Both. Simultaneously. Almost nobody could hold both thoughts, so one crowd got wiped out in the crash and the other missed the largest value creation event of the century.

Same test, new era.

Yes, parts of the AI trade will burn.

And the red line at the bottom of my chart — 1% of world GDP, growing faster than anything in economic history — will look like the blue line looks today: obvious, enormous, and owned by the people who stopped debating it in 2026 and learned to operate it instead.

The skeptics are writing think-pieces.

The believers are writing code.

In five years, check which group changed its wealth bracket.