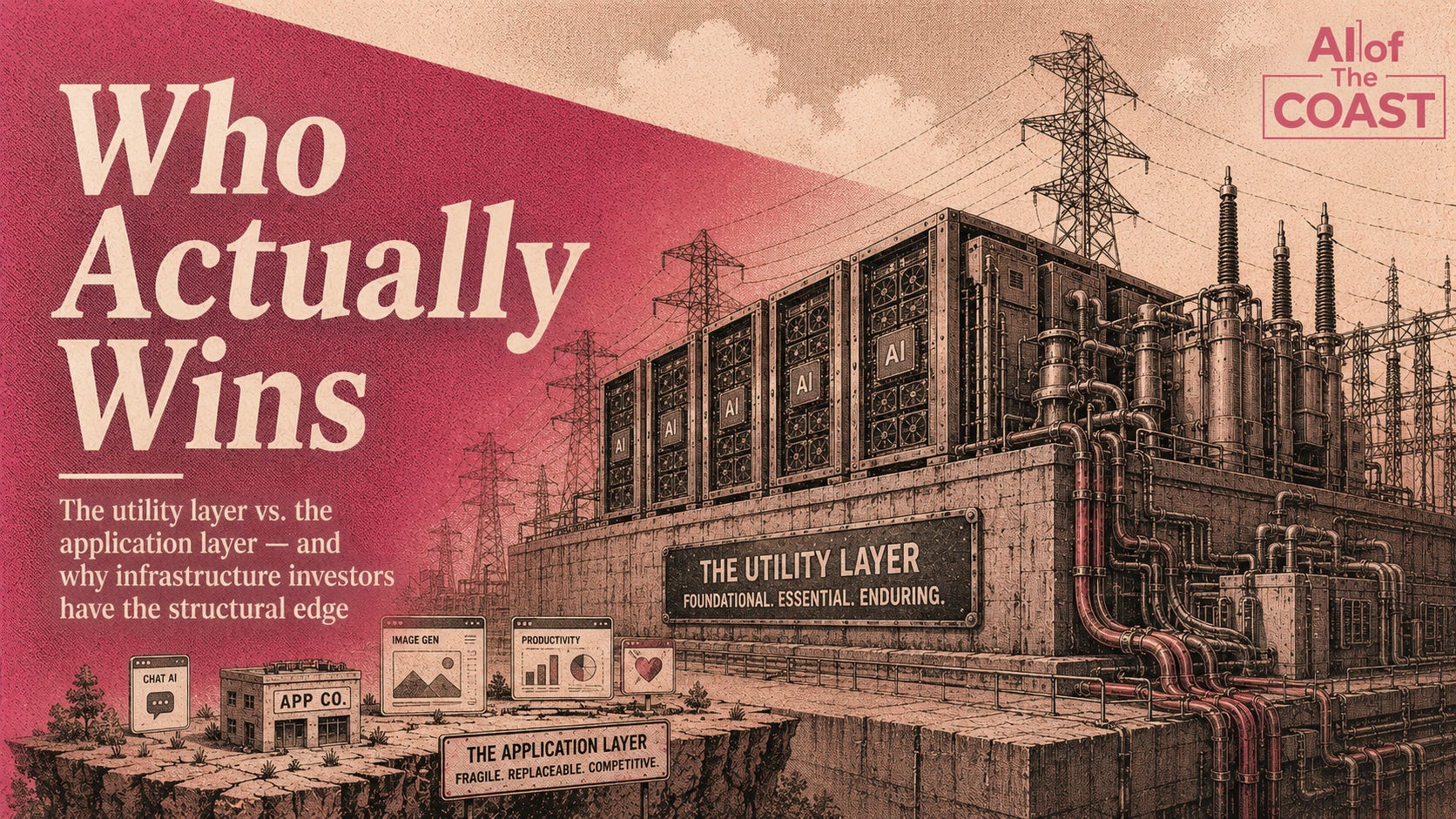

Who Actually Wins: The Utility Layer vs. the Application Layer

Every technology transition produces two investment narratives: the application layer story and the infrastructure layer story. . The infrastructure layer captures the economics.

Let me start with the historical record, because it is unambiguous. The internet created extraordinary wealth. The fiber optic infrastructure that made the internet possible — WorldCom, Global Crossing, 360networks — destroyed enormous amounts of investor capital in the collapse of 2000-2002. The companies that captured the internet’s economic value — Google, Amazon, Facebook, Netflix — came after the infrastructure was already built and largely written off.

Does this historical analogy mean AI infrastructure is a bad investment? It does not. The lesson of the fiber collapse is not “infrastructure is bad” — it is “infrastructure financed with the wrong capital structure at the wrong moment in the adoption curve is bad.” The fiber that was written off in 2002 carried the internet traffic that made Amazon and Google possible. The infrastructure was right. The timing and balance sheet were wrong.

Why This Infrastructure Cycle Is Structurally Different

The fiber collapse was driven by a specific confluence: massive capital investment ahead of demand that took 5-7 years longer to materialize than projected, financed with high-yield debt that required cash flow servicing before the demand arrived. When demand didn’t materialize on schedule, the capital structure collapsed even though the infrastructure itself was eventually proven necessary.

The AI infrastructure cycle has several structural differences that change the risk profile. First, demand is already materializing — not at full scale, but at accelerating scale with clear trajectory. The IEA reports data center electricity consumption grew 17% in 2025. That is not speculative. Second, the primary capital allocators in the current buildout are not leveraged startups — they are Microsoft, Google, Amazon, Meta, and Oracle, operating from strong balance sheets with the ability to absorb timing risk. Third, the workload characteristics of AI create stickier demand than internet bandwidth did: switching costs are higher, workload criticality is higher, and the regulatory environment is creating durable barriers.

“The question is not infrastructure vs. applications. The question is: which infrastructure, at what point in the adoption curve, with what capital structure? The answer determines whether you end up like WorldCom or Eaton Power.”

The Utility Economic Model

The strongest case for AI infrastructure investment is the utility economic model — the same model that makes electric utilities, water utilities, and telecommunications carriers some of the most durable businesses in the world. Utilities have three characteristics that compound over time: recurring revenue from metered consumption, high switching costs for customers once connected, and pricing power derived from being a critical input to economic activity.

AI compute is acquiring all three. Cloud computing revenue is already almost entirely recurring, contract-based, and consumption-metered. Customers who have integrated AI into production workflows have switching costs that grow with the depth of integration. And compute is increasingly non-optional for organizations competing in an AI-native economy — which means pricing power accrues to whoever has the available capacity.

The infrastructure operators who position themselves as utilities — providing metered AI compute capacity, building durable customer relationships through SLAs and integration depth, and deploying capital at the bottleneck points in the supply chain (energy, high-density facilities, cooling) — are the ones with the most defensible long-term economic position.

The Application Layer Is Highly Competitive, Rapidly Commoditizing

The contrast with the application layer is stark. The AI model market is intensely competitive, with Anthropic, OpenAI, Google DeepMind, Meta AI, and Mistral all competing at the frontier. Inference costs per token have fallen by roughly 99% since GPT-3’s debut in 2020. API prices continue to decline. The application layer is being commoditized from below by open-source models and from above by hyperscaler bundling.

This is not an argument that application companies are bad businesses. It is an argument that their economic moat is narrower than widely perceived, and that the infrastructure layer — power, cooling, compute delivery — has a more durable competitive position by virtue of the capital intensity, long development timelines, and scarcity of appropriately-zoned, powered sites.

The operators building modular, energy-first AI infrastructure today are not guaranteed to win. Infrastructure investments can and do fail. But the structural economics — recurring revenue, high switching costs, scarcity of appropriately powered sites, and exposure to an adoption curve that is in its earliest innings — represent exactly the kind of asymmetric infrastructure bet that has historically produced the most durable returns in technology transitions.